Sales activity in prime London remained slow in March, with transactions remaining lower than last year despite an increase in new listings, according to analysis by Loanres.

Sales activity in prime London remained slow in March, with transactions remaining lower than last year despite an increase in new listings, according to analysis by Loanres.

There were 41% fewer sales in March compared to the same month in 2025, and transactions were also 13.3% below the pre-pandemic average for the time of year. While last year’s figures were boosted by the stamp duty deadline, activity in 2026 remains weak by long-term standards.

New orders increased 8.8% year over year and were well above pre-pandemic levels, leading to a 13.8% annual increase in available stocks. However, the increase in supply has not translated into full sales, with agreed deals taking longer to move through the exchange.

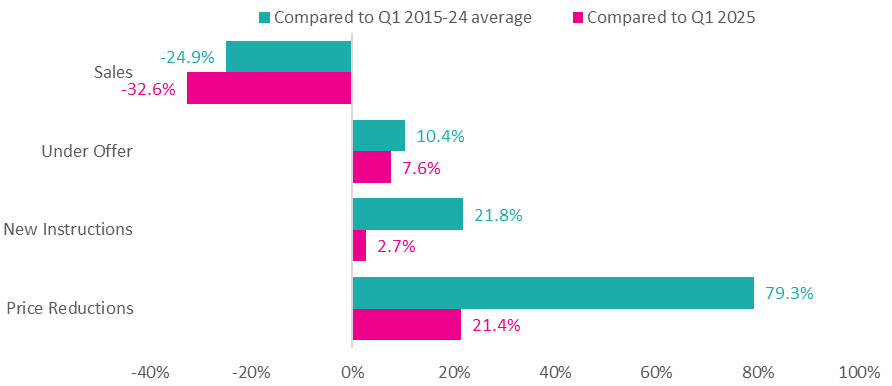

The number of properties coming under offer has increased by more than 21% compared to a year ago, suggesting buyer interest remains, but transaction volumes have still not recovered.

Prices also remained under pressure. The average realized selling price in March declined 5.5% year-on-year and was 7.5% below pre-pandemic levels. Discounts have become more pronounced, with the average sale agreed at 10.5% below the initial asking price.

Activity in the super-prime market followed a similar pattern. Transactions for homes priced over £5 million were down 3% from a year earlier, while the number of such properties available for sale increased by 7.2%.

Overall in the first quarter, sales volumes were down nearly a third compared to 2025 and about a quarter below the long-term average.

In contrast, the prime lettings sector showed signs of improvement. Average rents rose 0.3% year-over-year in March, marking a return to growth after three consecutive monthly declines.

Lettings activity increased rapidly, with the number of agreed lettings increasing by 36.3% compared to a year ago and new rental instructions increasing by 61.7%. The supply of rental properties also expanded, with stock levels increasing by 48.4% year-on-year.

Nick Gregory, head of research at Loanres, said: “March is typically a busy time for the market, and feedback from agents confirms that buyers are starting their searches and heading out on viewings.

“Our latest data shows this is starting to translate into more agreed offers – the year-on-year figure is 7.6% higher than in 2025 – but sales volumes remain significantly low, with various issues limiting the flow of deals through the full transaction process.”

Gregory said: “Looking ahead, global uncertainty and a weak domestic economy means confidence is low in general. This limits the activity of those who do not ‘need’ to move and limits the movement of those who are still willing to pay in the market.

“Purchasing power has been further eroded by rising mortgage rates and withdrawal of deals in response to inflation fears due to the conflict in Iran. At the time of writing, the situation there appears to be easing, but this could change rapidly again.”