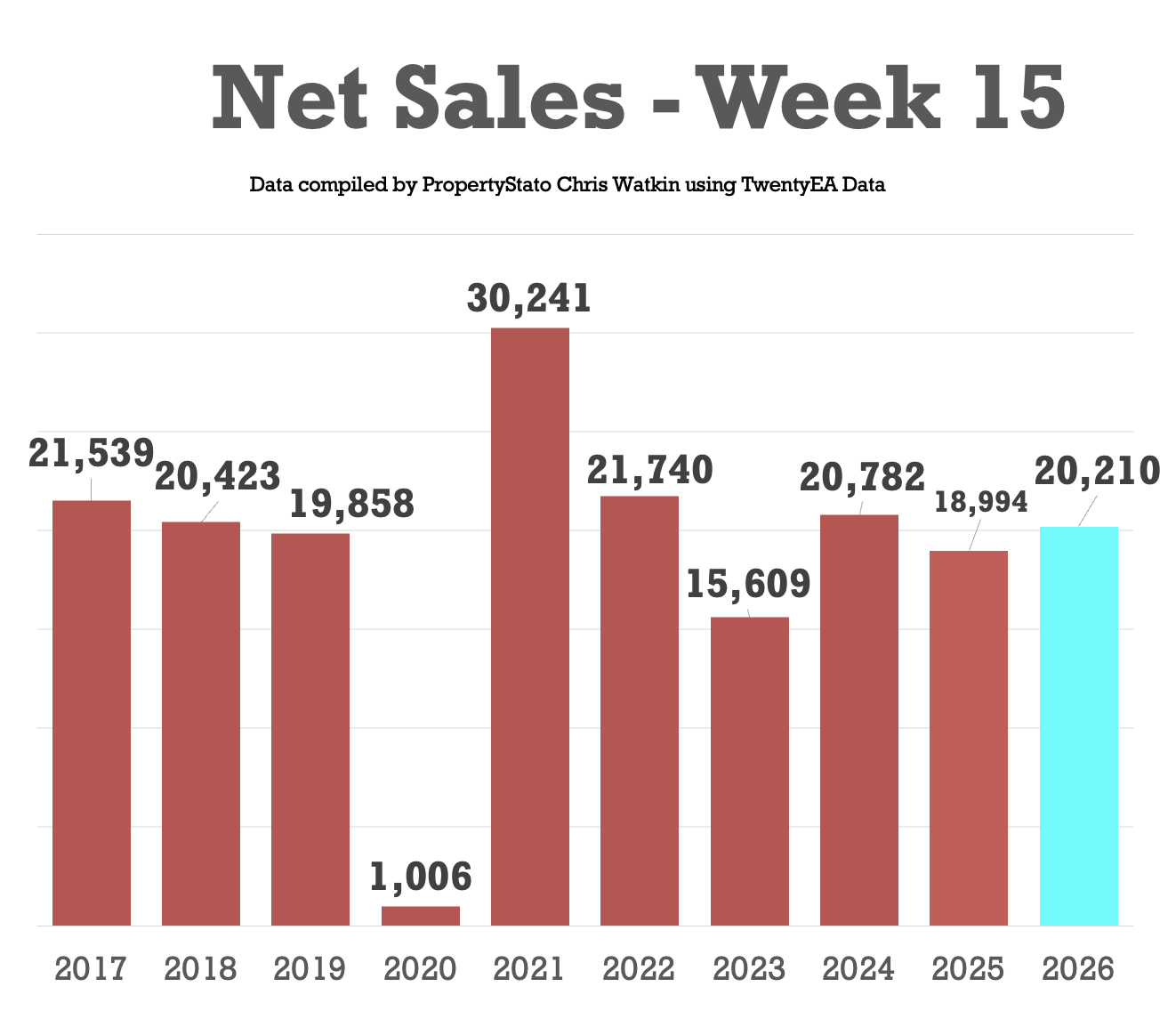

On this week’s UK Property Market Stats Show, I’m joined by Ben Madden to break down the market for the week ending Sunday 19 April 2026 (Week 15).

On this week’s UK Property Market Stats Show, I’m joined by Ben Madden to break down the market for the week ending Sunday 19 April 2026 (Week 15).

In the second half, we turn to the pool, analyzing which properties and letting agents are performing best – and why.

Even if you’re not in the pool, analytics will be familiar territory to agents dealing with competitors or fee-cutting competitors. We look at practical ways to prove performance, win instruction and justify strong fees.

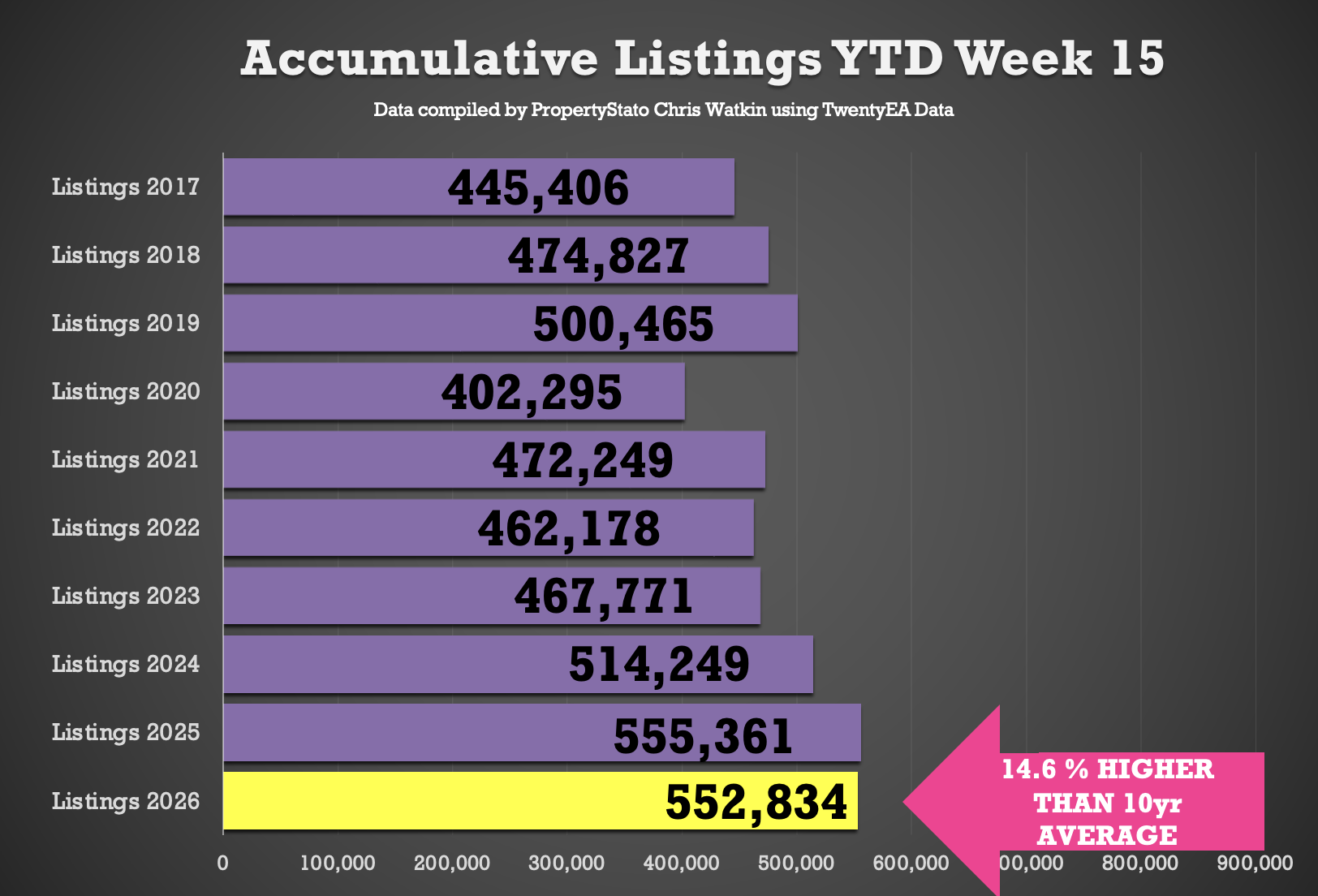

🟩 Listing YTD

553k new properties have come on the market YTD

0.5% lower than 2025 YTD, 7.4% higher than 2024 YTD, and 16.7% higher than the 2017-19 average YTD

🟧Total residential Sales YTD

368k UK homes sold STC YTD

6.7% lower than 2025 YTD (368k), 5.1% higher than 2024 YTD (350k), 16.1% higher than 2023 YTD (297k) and 12.1% higher than pre-Covid norms (303k).

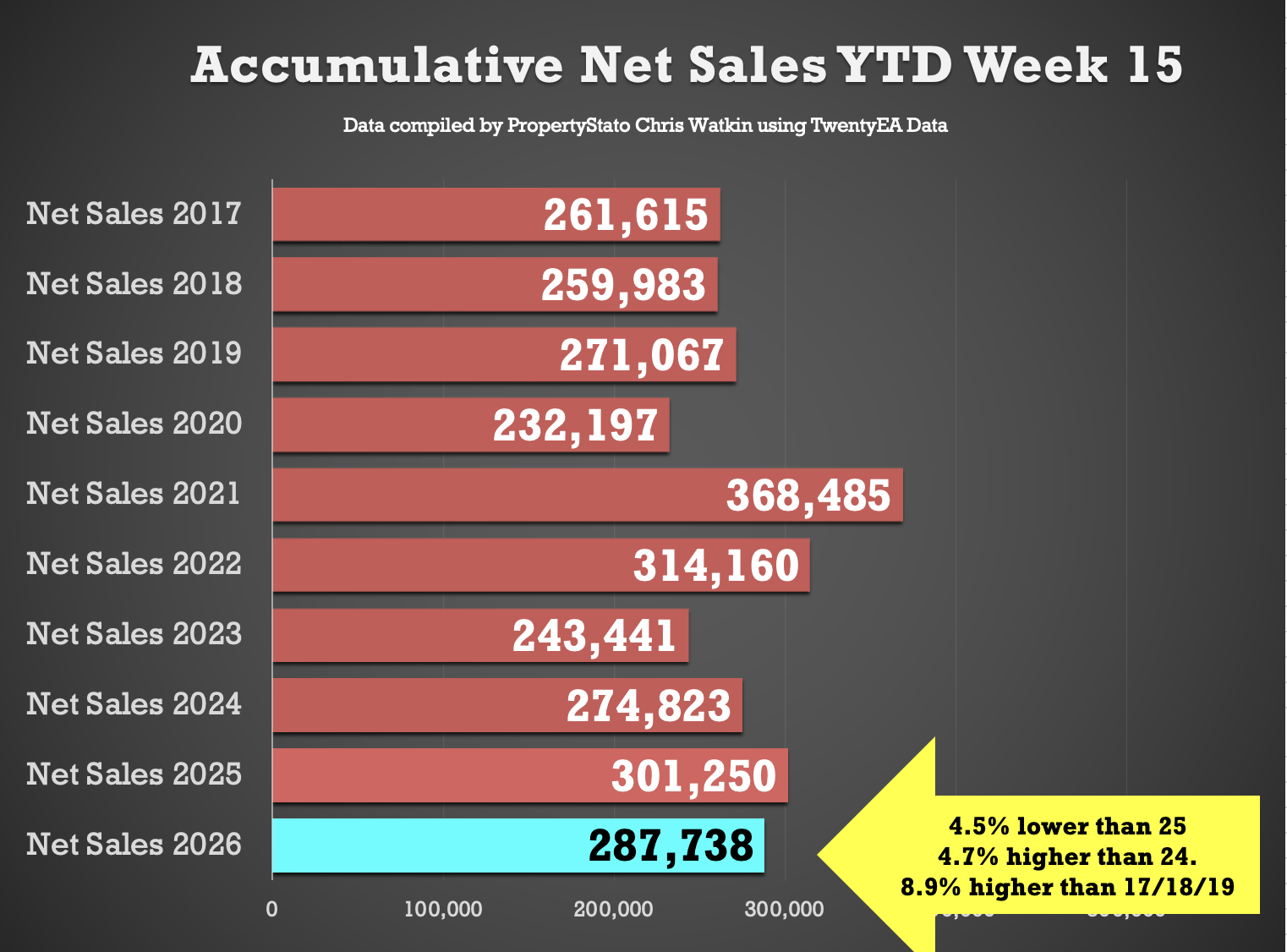

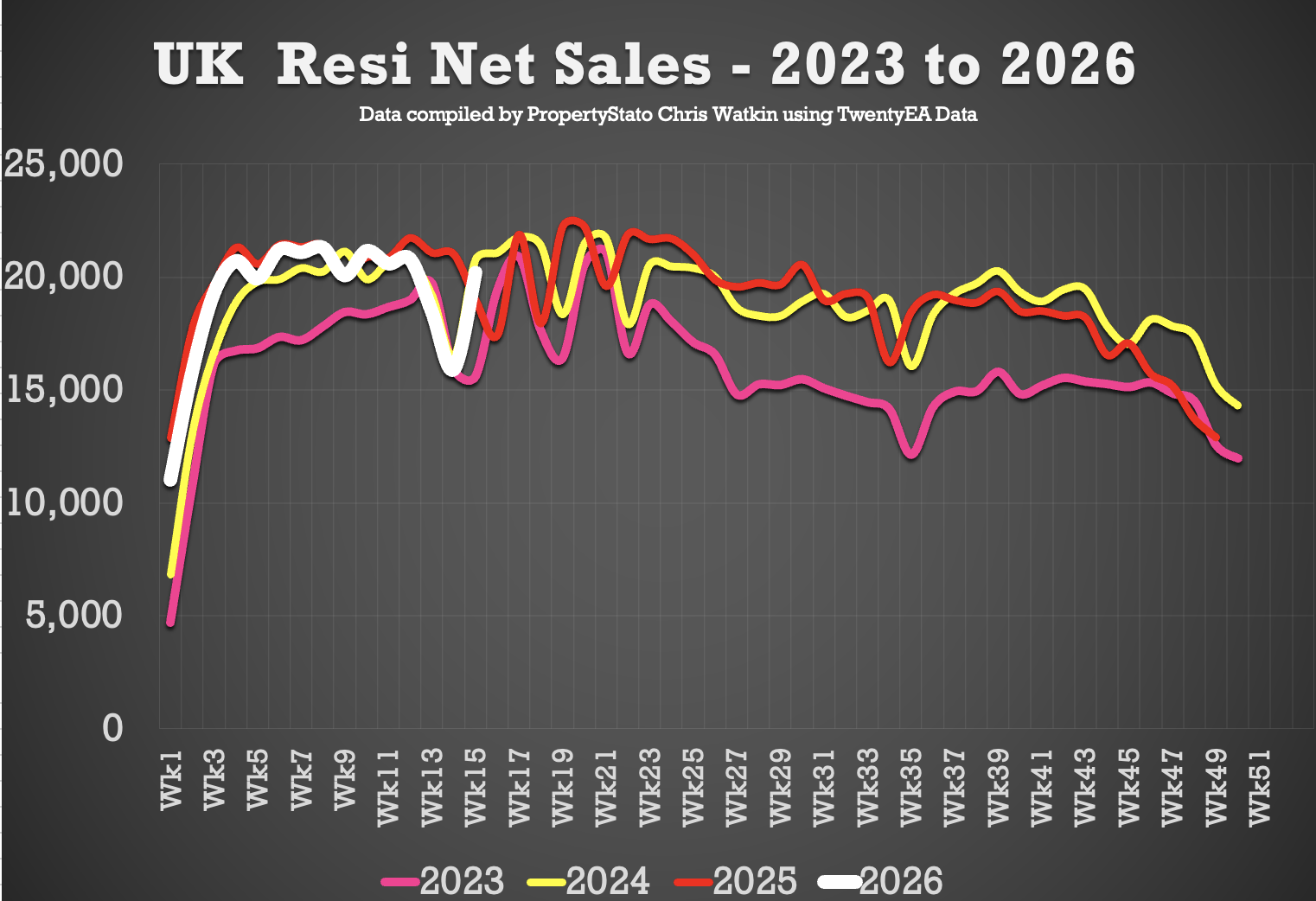

🟩 Net Res Sales YTD

288k UK net domestic sales YTD (net sales, gross sales less fall through).

4.5% below 2025 (301k), 4.7% ahead of 2024 (275k), 18.2% ahead of 2023 (243k) and 8.9% above the 2017-19 average (264k).

🟥 Exchange YTD

214k UK exchanges by end March 2026

13% lower than mid-March 2025, when it stood at 246k.

Note – More exchanges took place in Q1 2025 due to the stamp duty holiday ending in April 2025.

🟥 overestimate

47% of homes left on the books of UK estate agents in March were withdrawn unsold. Main reason – blatant overvaluing supported by 20+ week long sole agency agreements.

Detailed description…

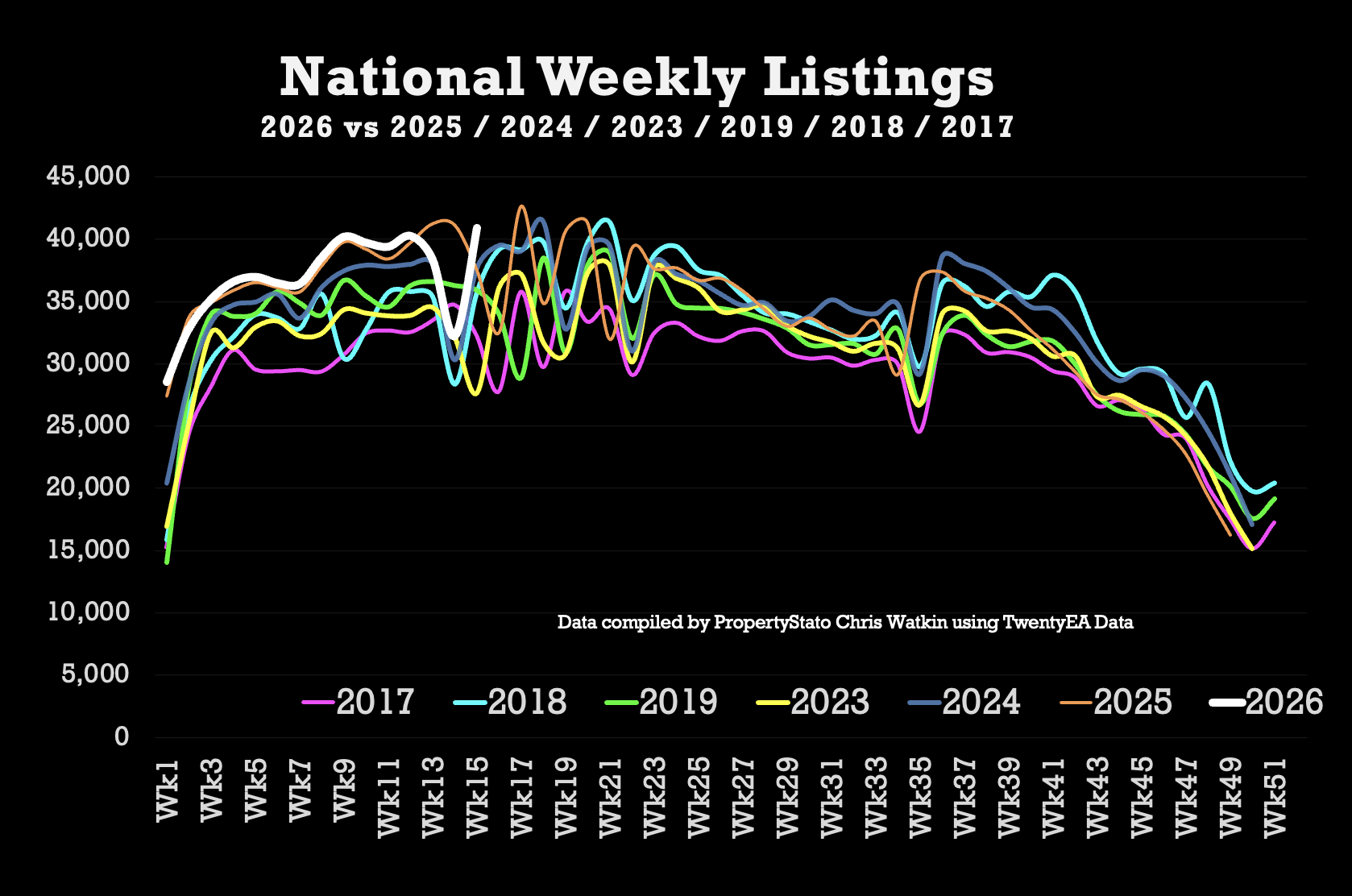

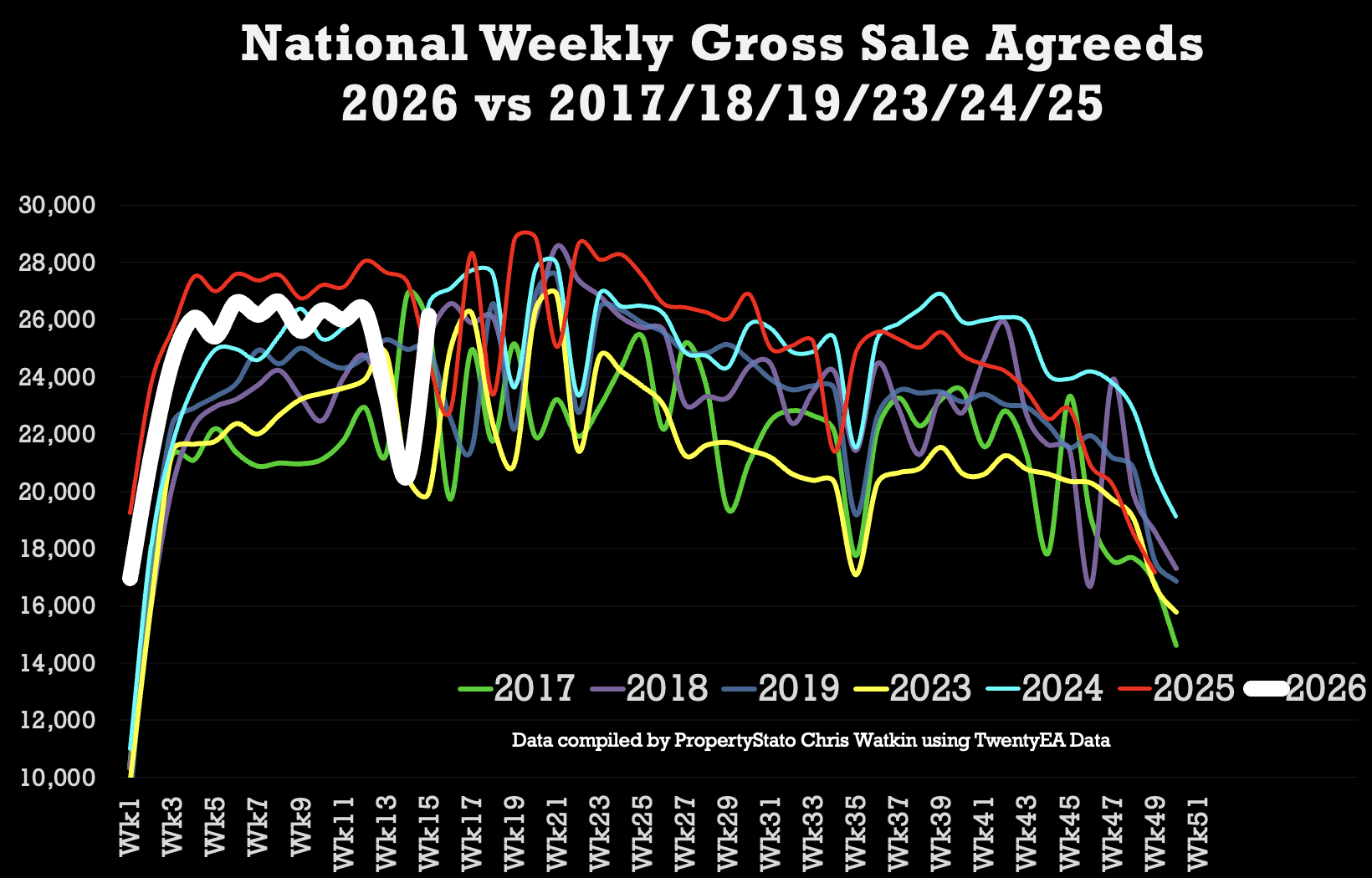

Remember, this is the first week after Easter week, so there is a big jump in most of the figures

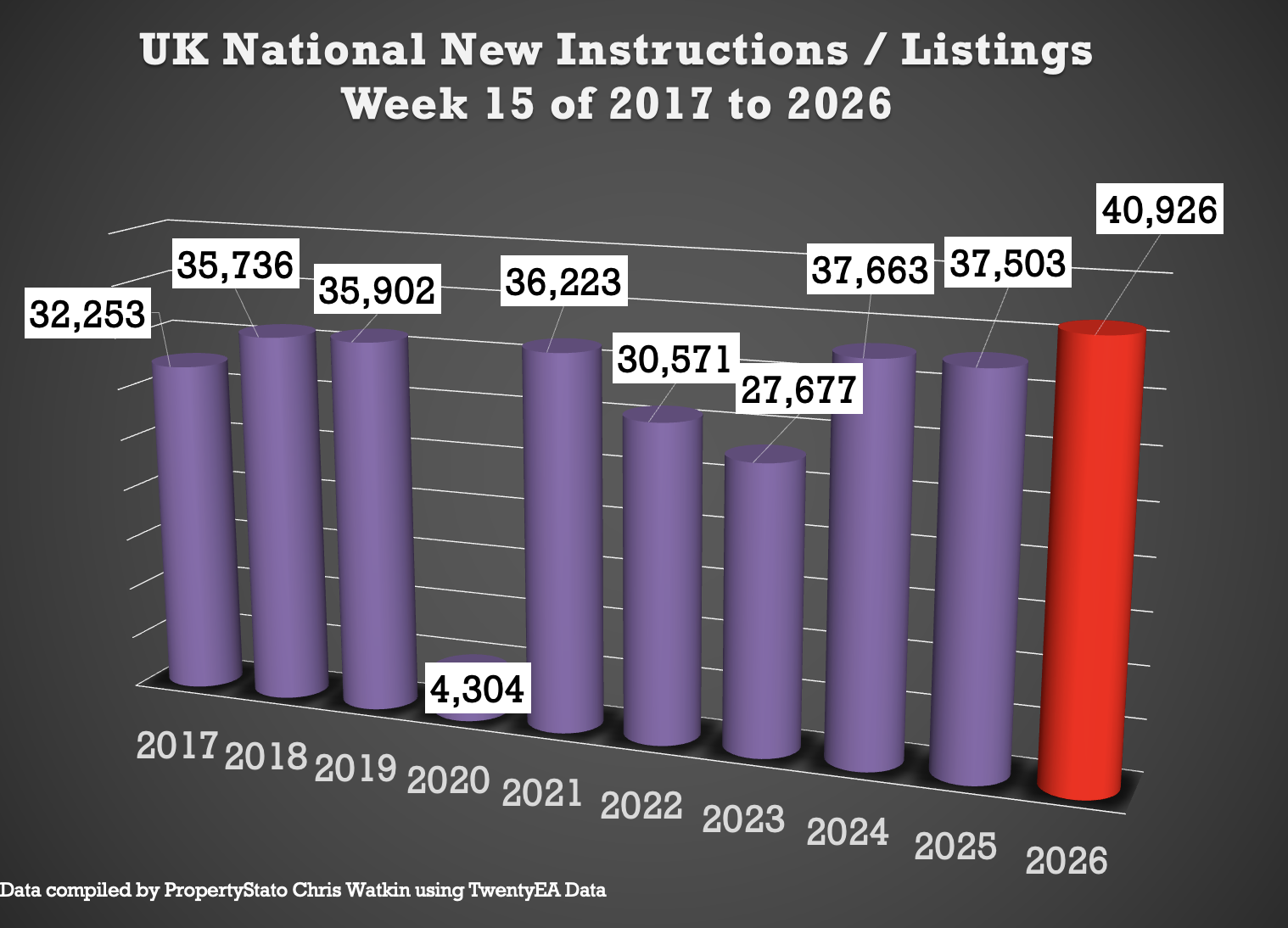

✅ new lists

• This week (Week 15) 41 thousand new properties came on the market, up from 32.2 thousand last week.

• 2025 weekly average: 30.6k.

• 10-Year Week 14 Average: 31.9K.

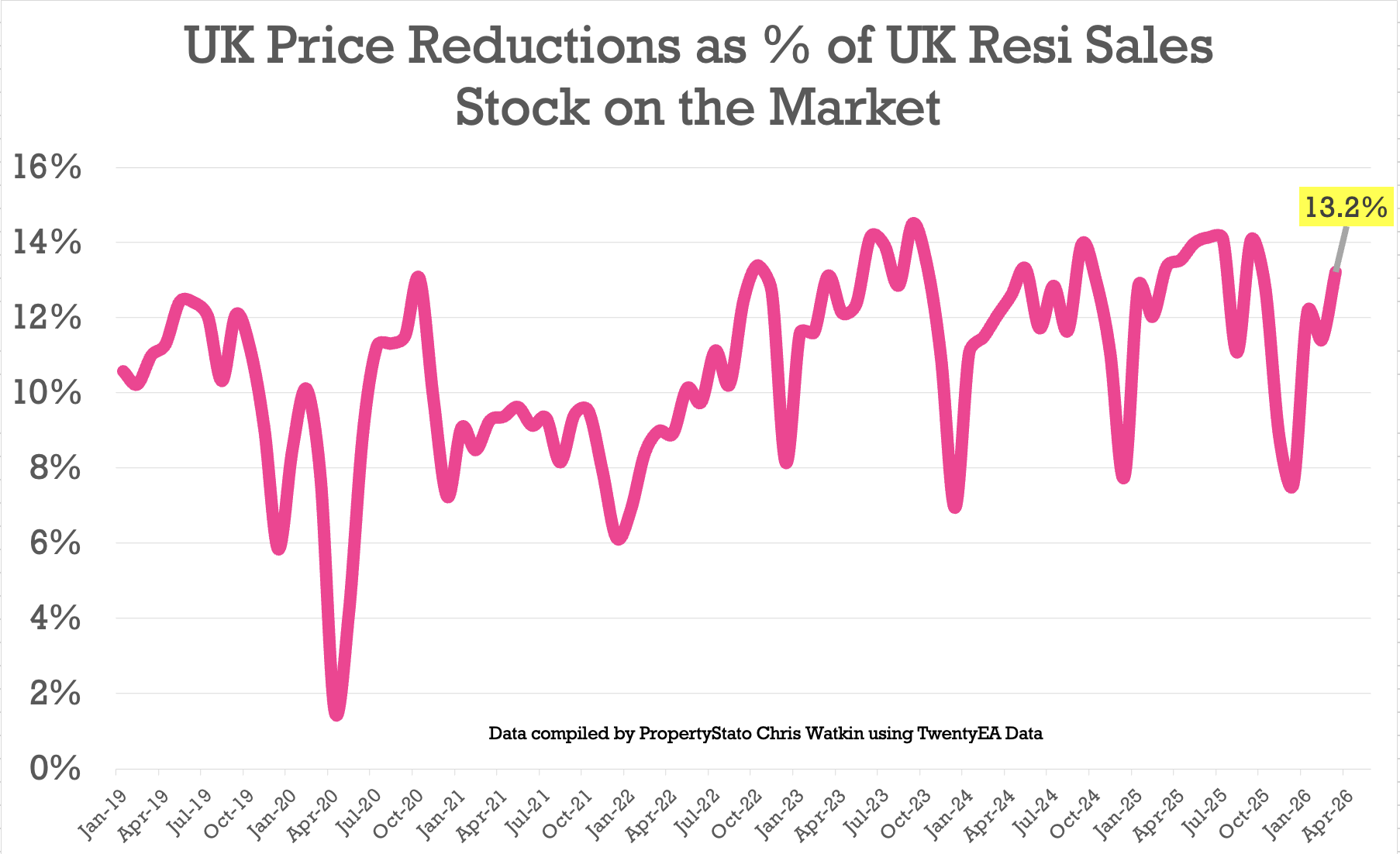

✅ price cut

• This week there was a cut of 25.6 thousand, which is less than 20.5 thousand last week.

• Sales of residential homes decreased by 13.2% in March. March 25 – 13.4%. March 24 – 12.2%

• The 2025 average was 12.8%, while the 6-year long-term average was 10.7%.

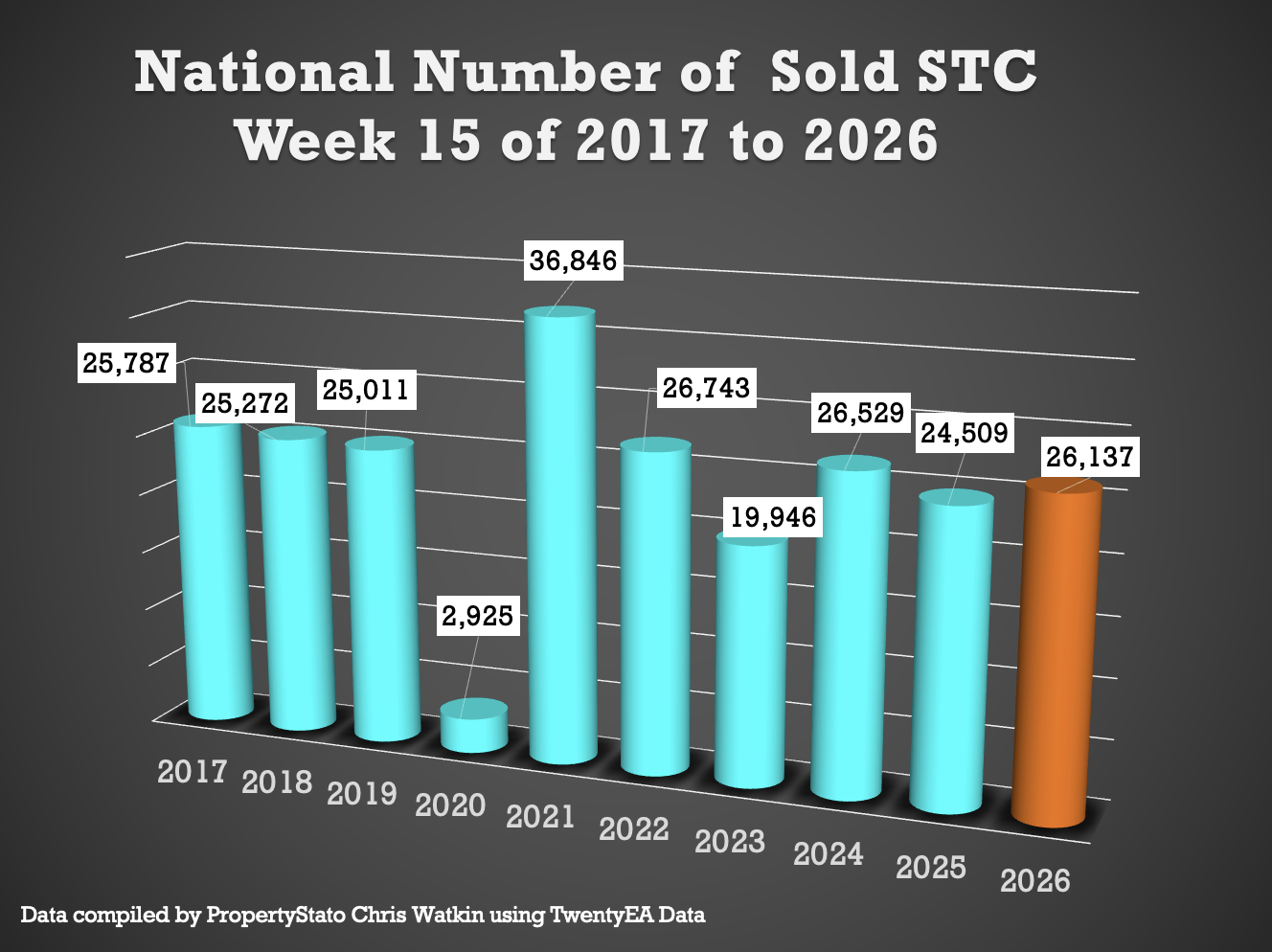

✅ consent to sale

• This week 26.1 thousand houses were sold in STC 15, which is more than 20.5 thousand last week.

• Week 15 average (for the last 10 years including post-pandemic surge): 24K

• 2026 weekly average: 24.4k.

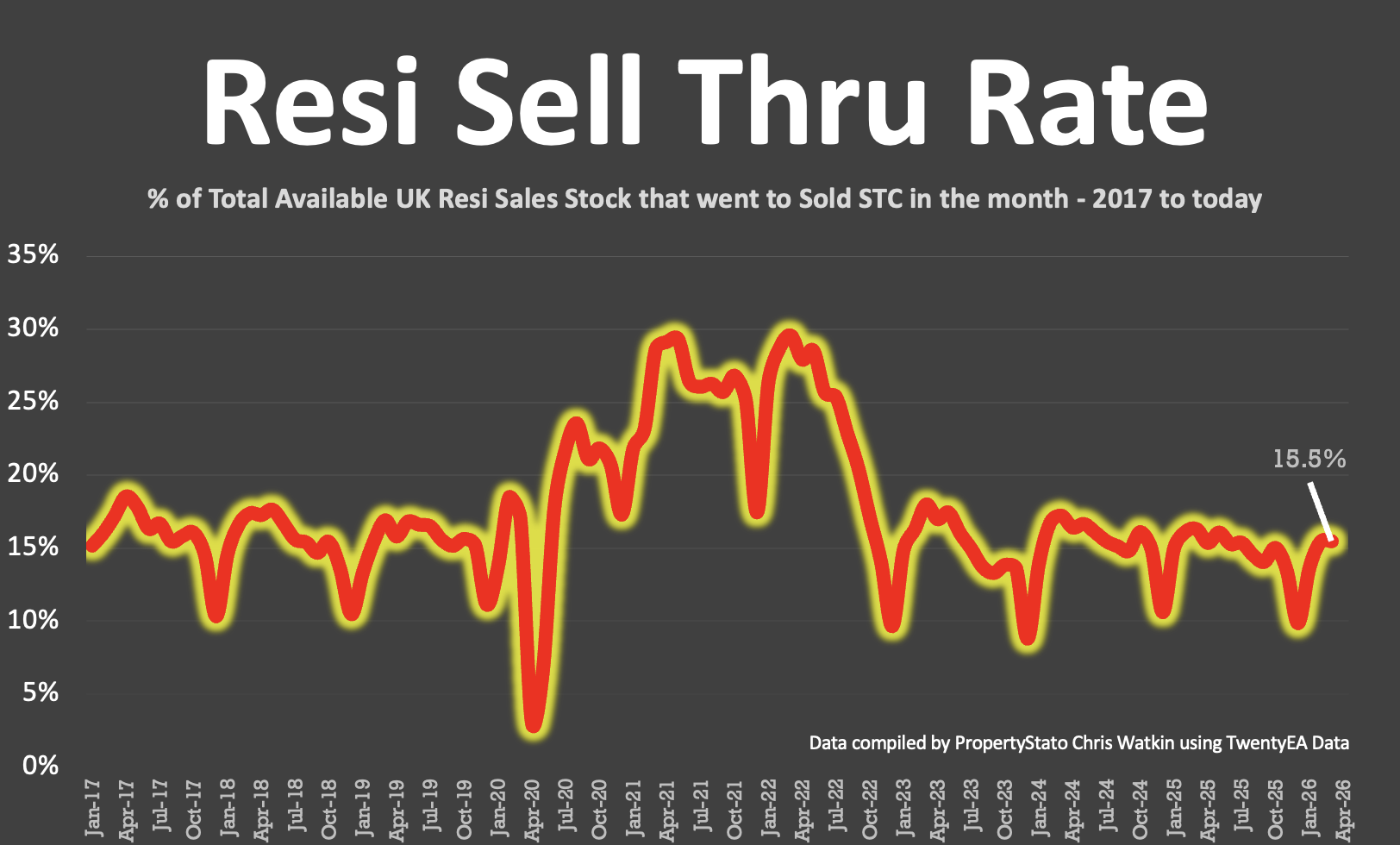

✅ sell-through rate

• 15.5% of homes on agents’ books moved to SSTC in March ’26. (Mar ’25 – 16.3% / Mar ’24 – 17.2%)

• Pre-Covid average: 15.5%.

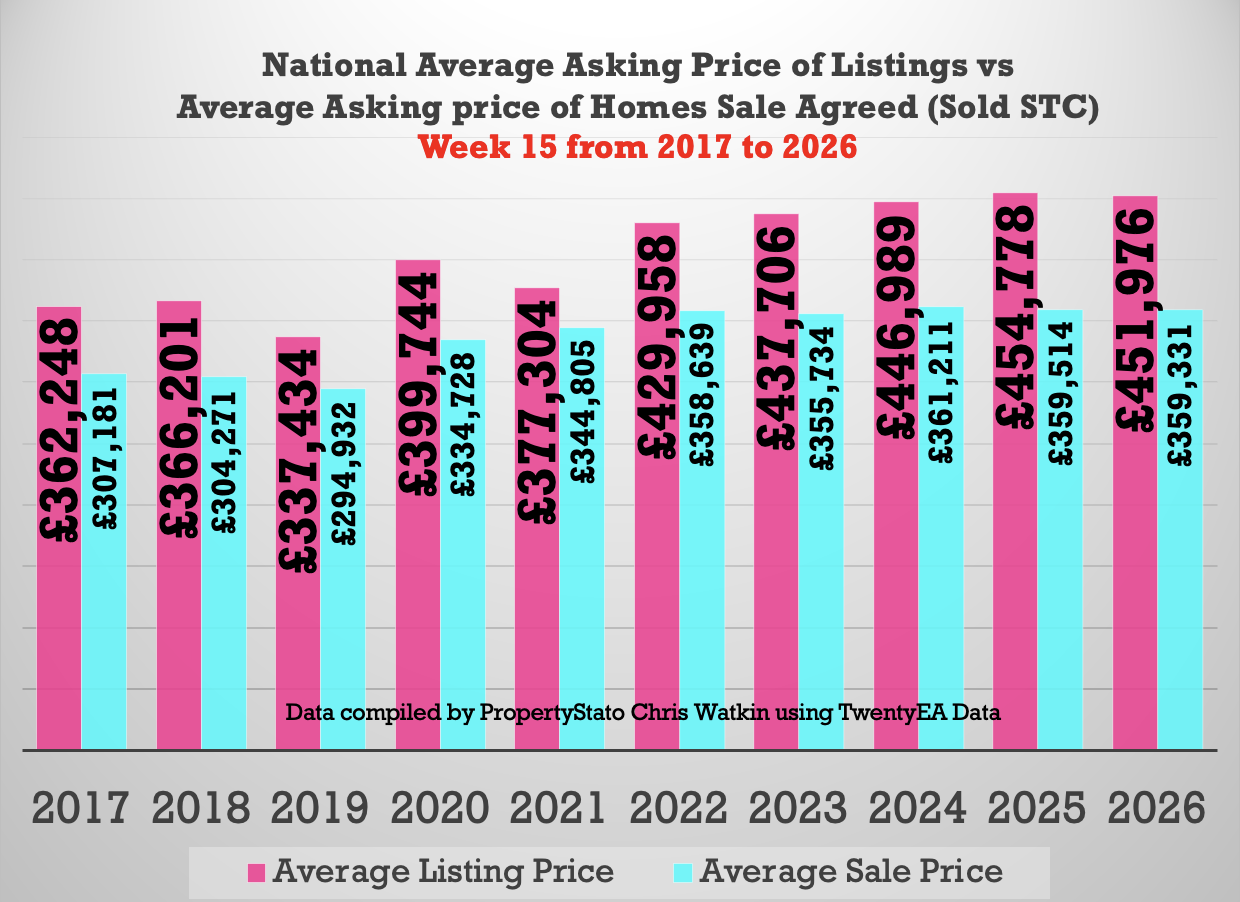

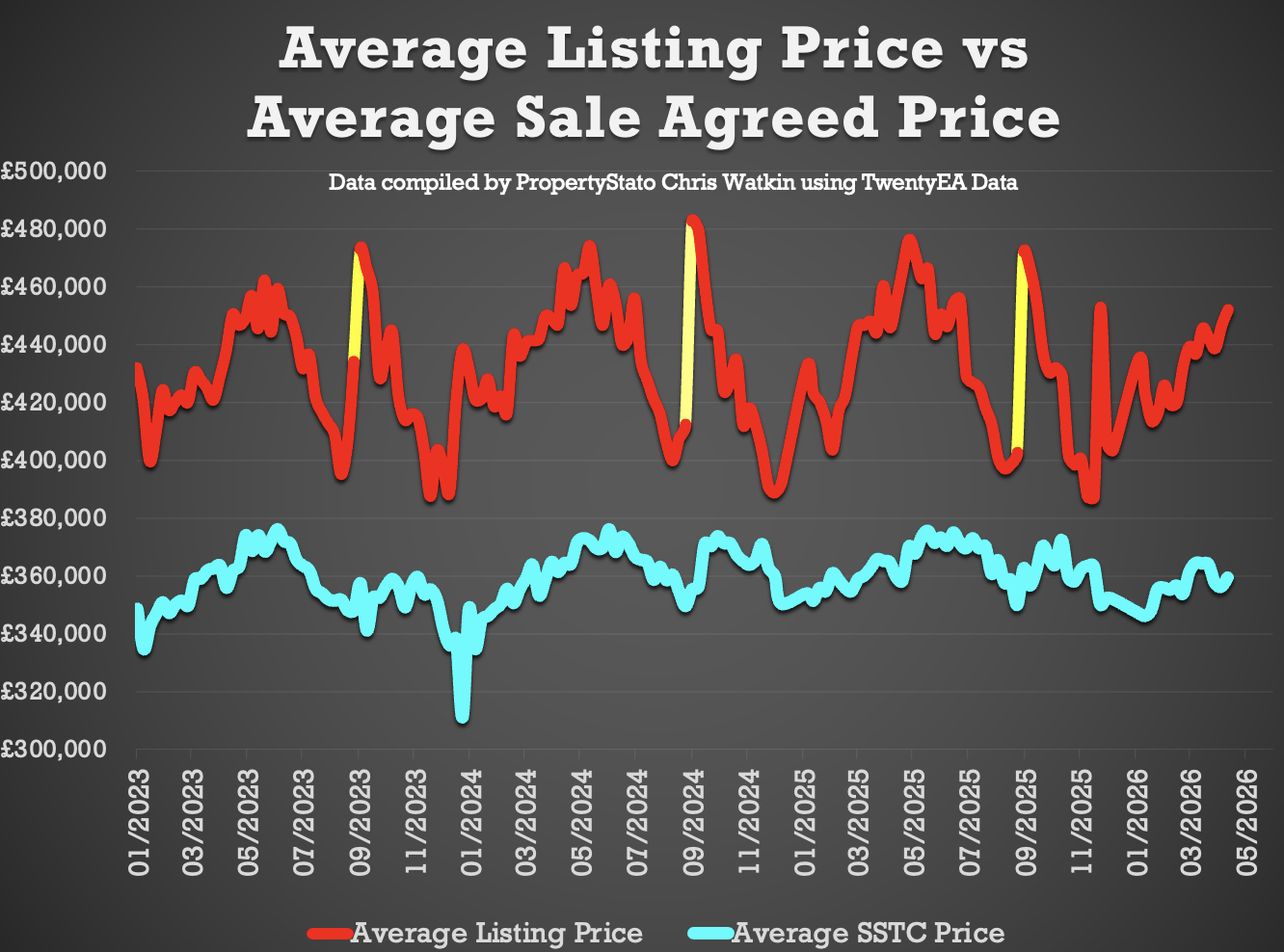

✅ Price difference between listing and sale

• 25.8% difference (long-term 10-year average is 16% to 17%). (£451k ave listing ave asking price vs £359k sale agreed ave asking price).

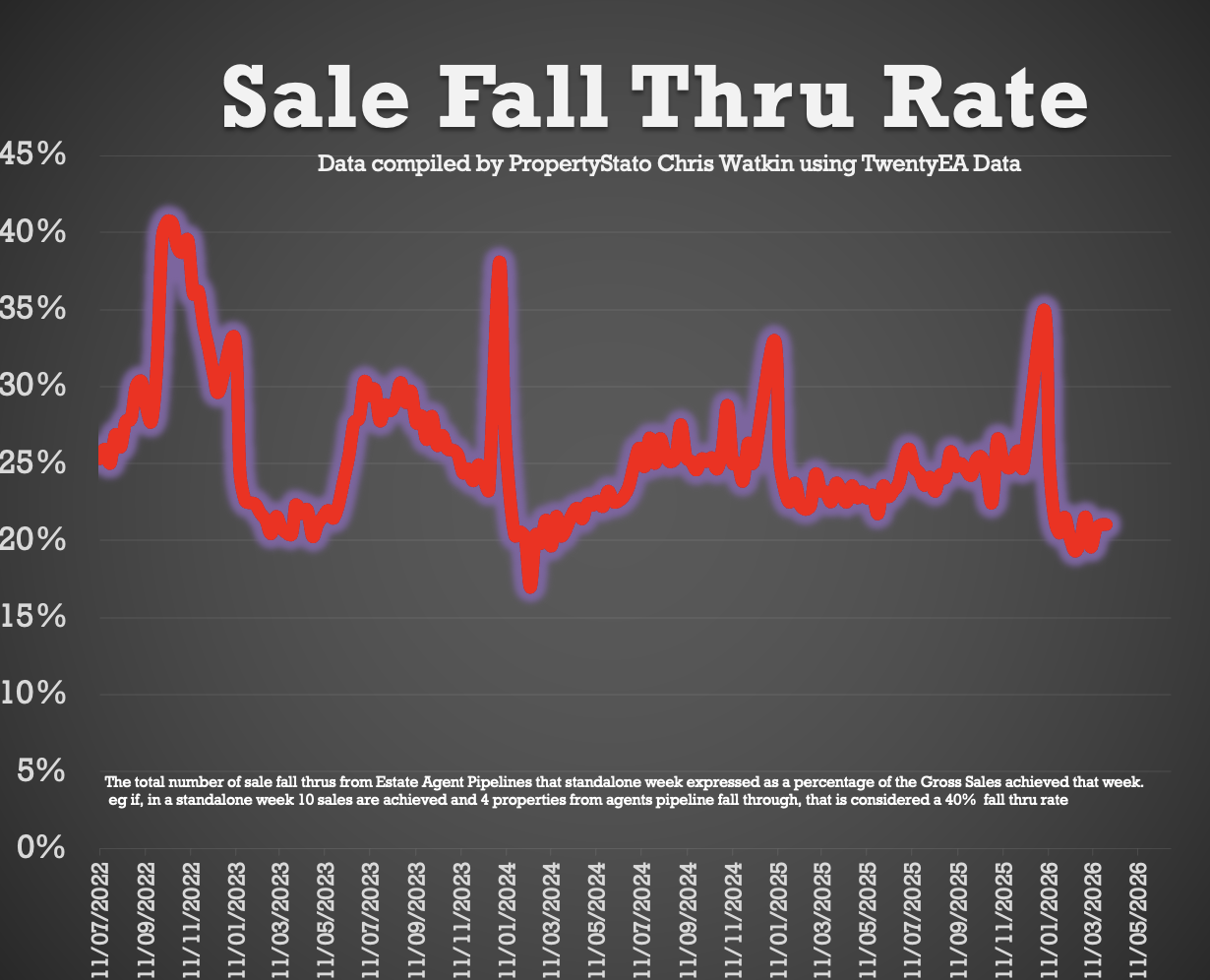

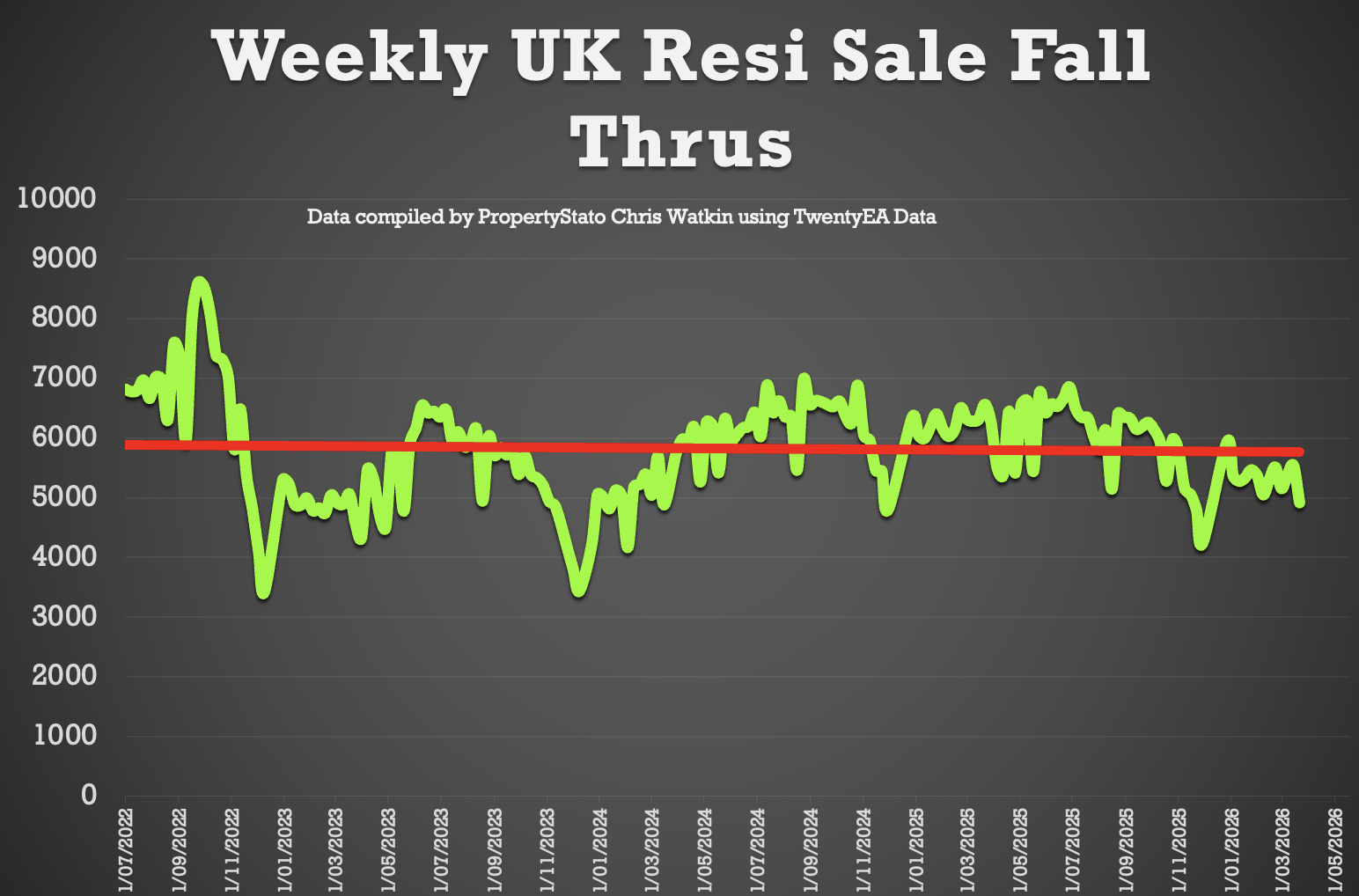

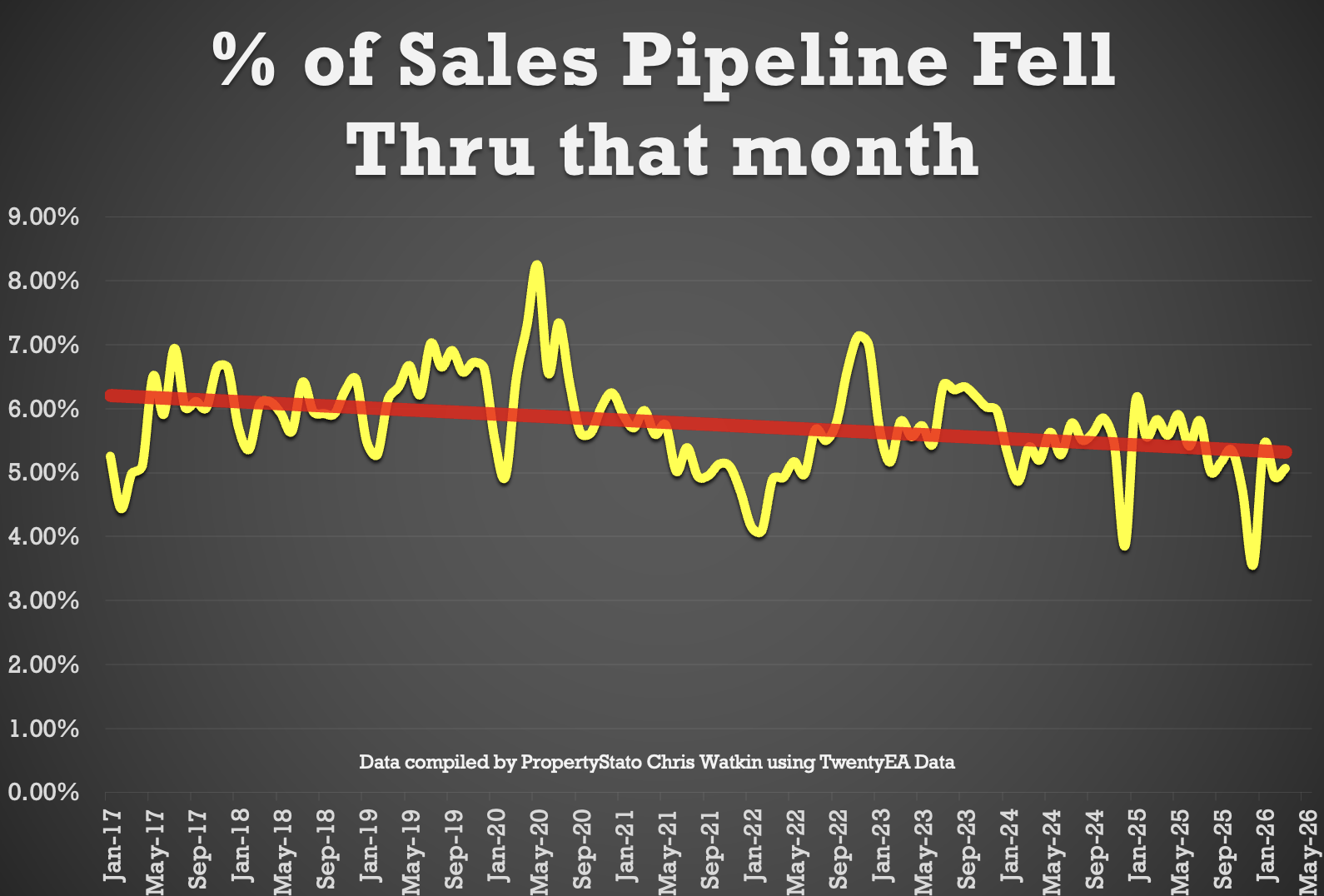

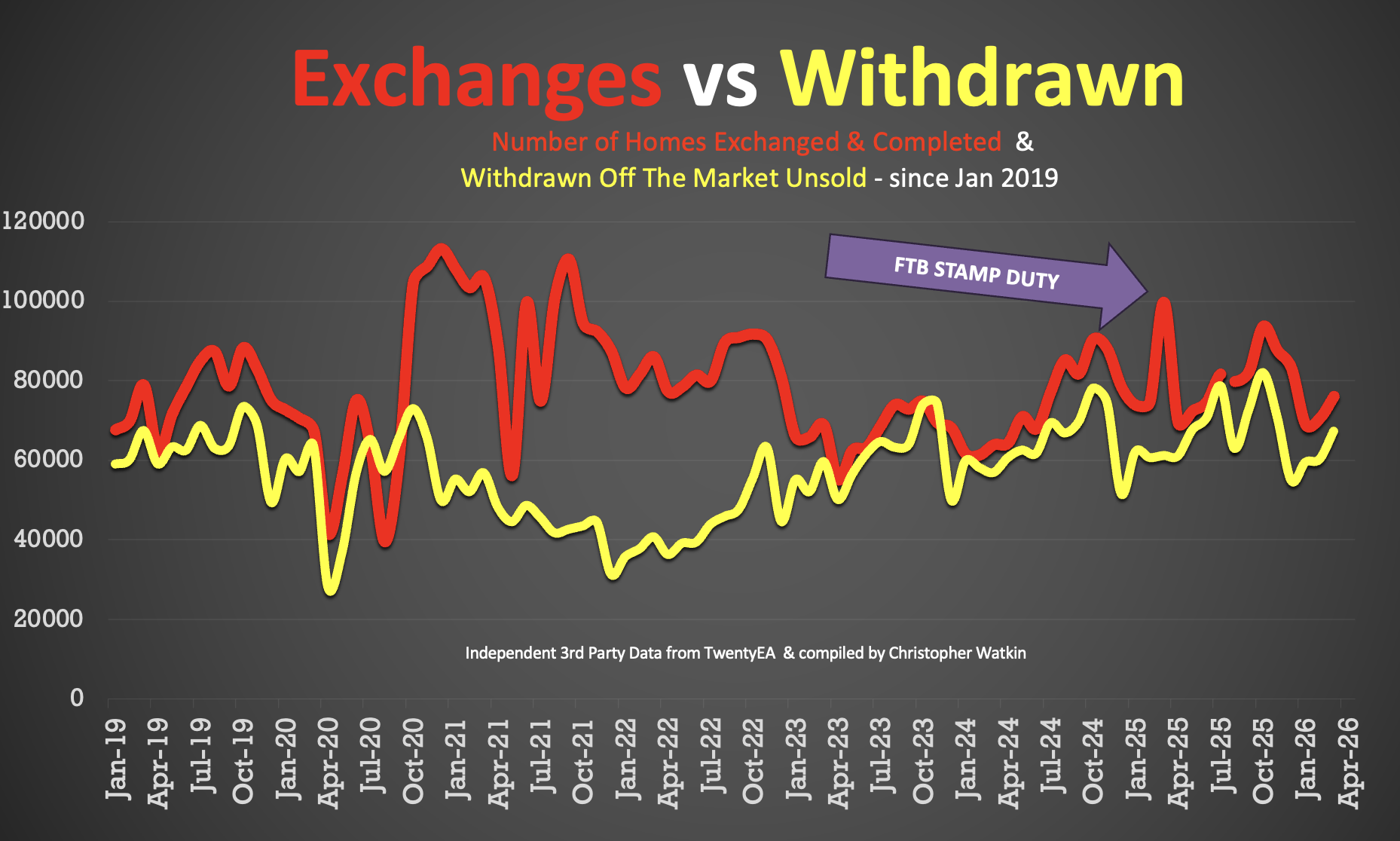

✅ fall-through

• 5,927 fall-throughs last week (STC’s pipeline sold 453k homes).

• Weekly average of decline till 2025: 6.1k And 5.3k in 2026 YTD

• Fall-through rate (fall-through expressed as a % of gross sales for that week): 25.8%Up 22.5% from last week.

• Long term average: 24.5% (post-truce anarchy levels seen above 40%).

• Estate agent sales pipelines fell by 5.1% of all sales agreed in March 2026. 2025 average – 5.3% and 10 year average – 5.8%).

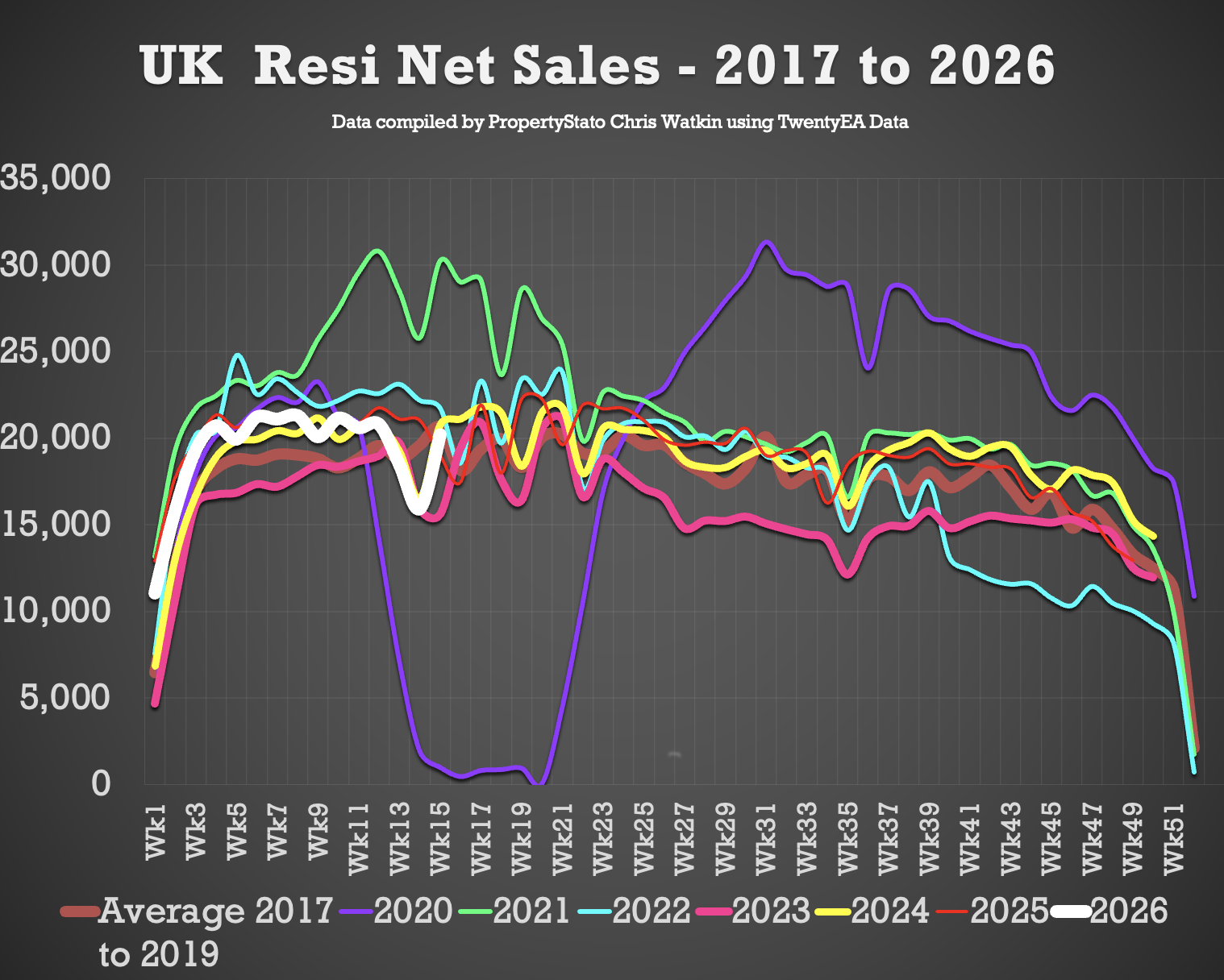

✅ total sales

• 16k net sales, down from 18.5k last week

• Ten-year Week 14 average: 17.8k.

• Weekly average for 2026: 19.1k.

• Weekly average for all of 2025: 18.8k.

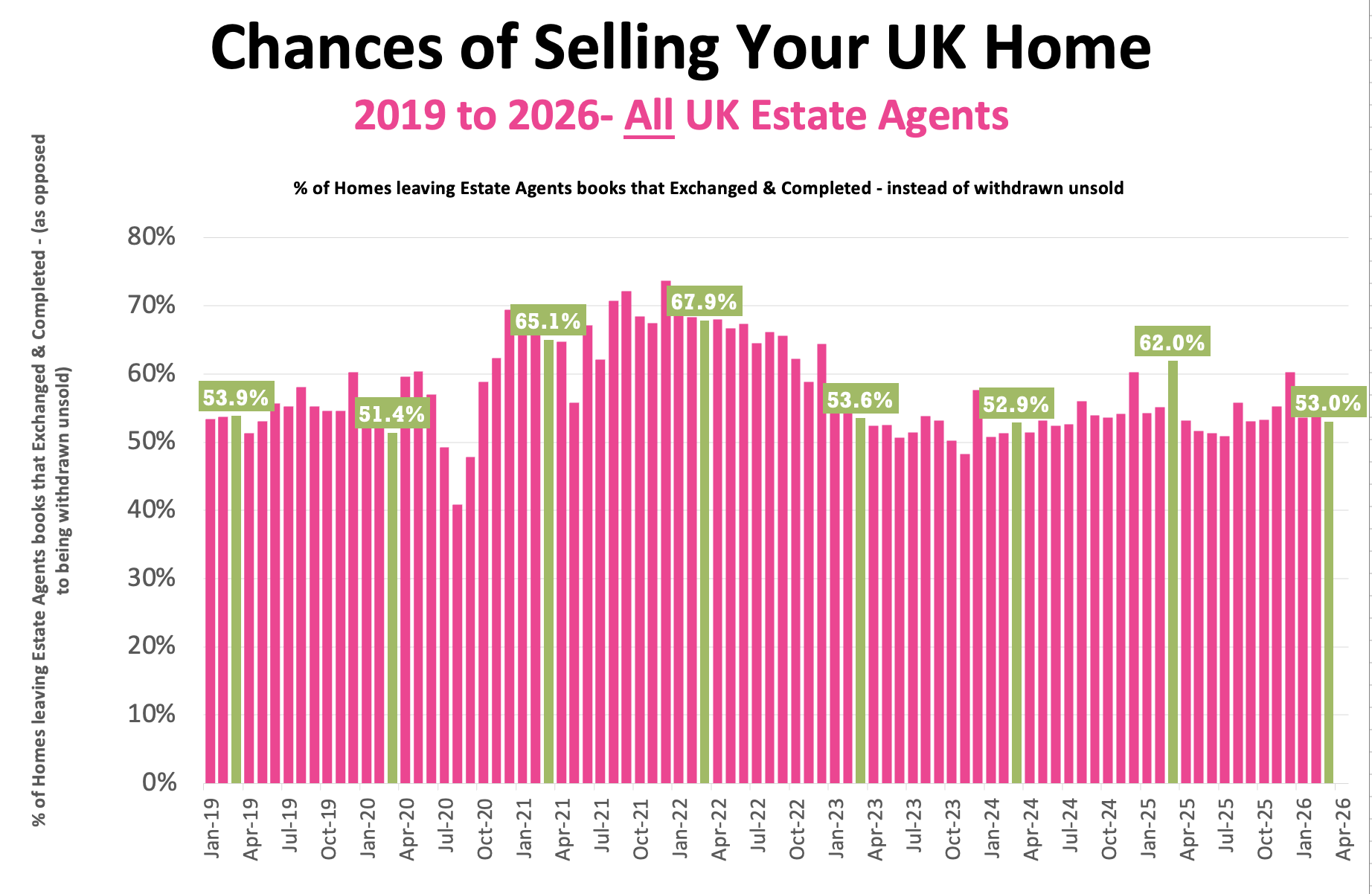

✅ Probability of Selling (% of Exchange vs. Withdrawal)

• March ’26 stats: 53% of homes exchanged and completions on agents’ books were completed in March. (Note that this figure will change throughout the month as more March data becomes available).

• 57.6% is a 7-year average (which includes the crazy 18 months following the lockdown).

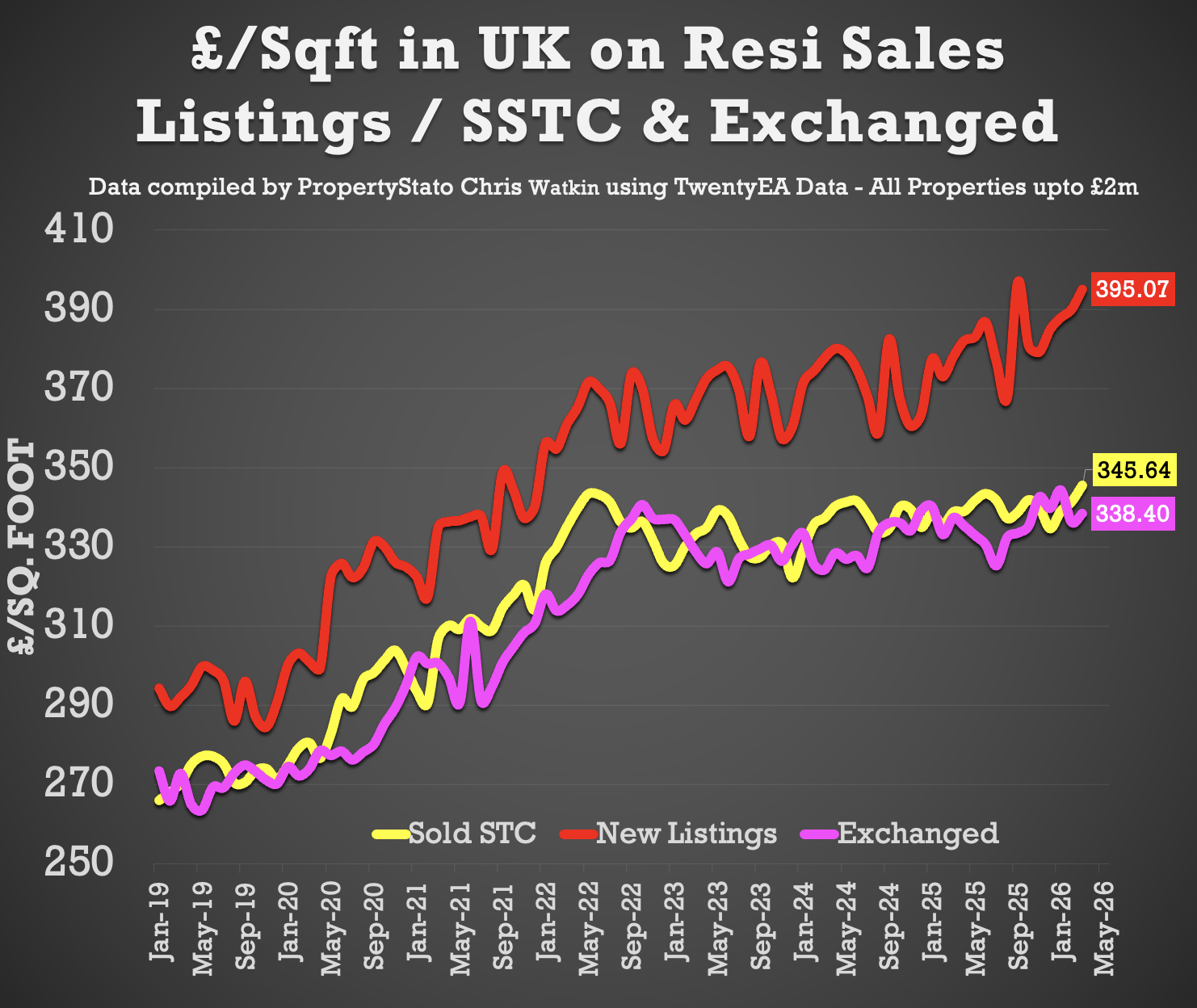

✅ House prices (£/sq ft)

• Agreed sales in March ’26 averaged £345.64 per square foot. Up 2% from 12 months ago (£338.97) and 12.7% up from 5 years ago (£306.76). Sale agreed £/sqft, matches HM Land Registry index with 98% accuracy 5 months ago. That’s why it’s so important.

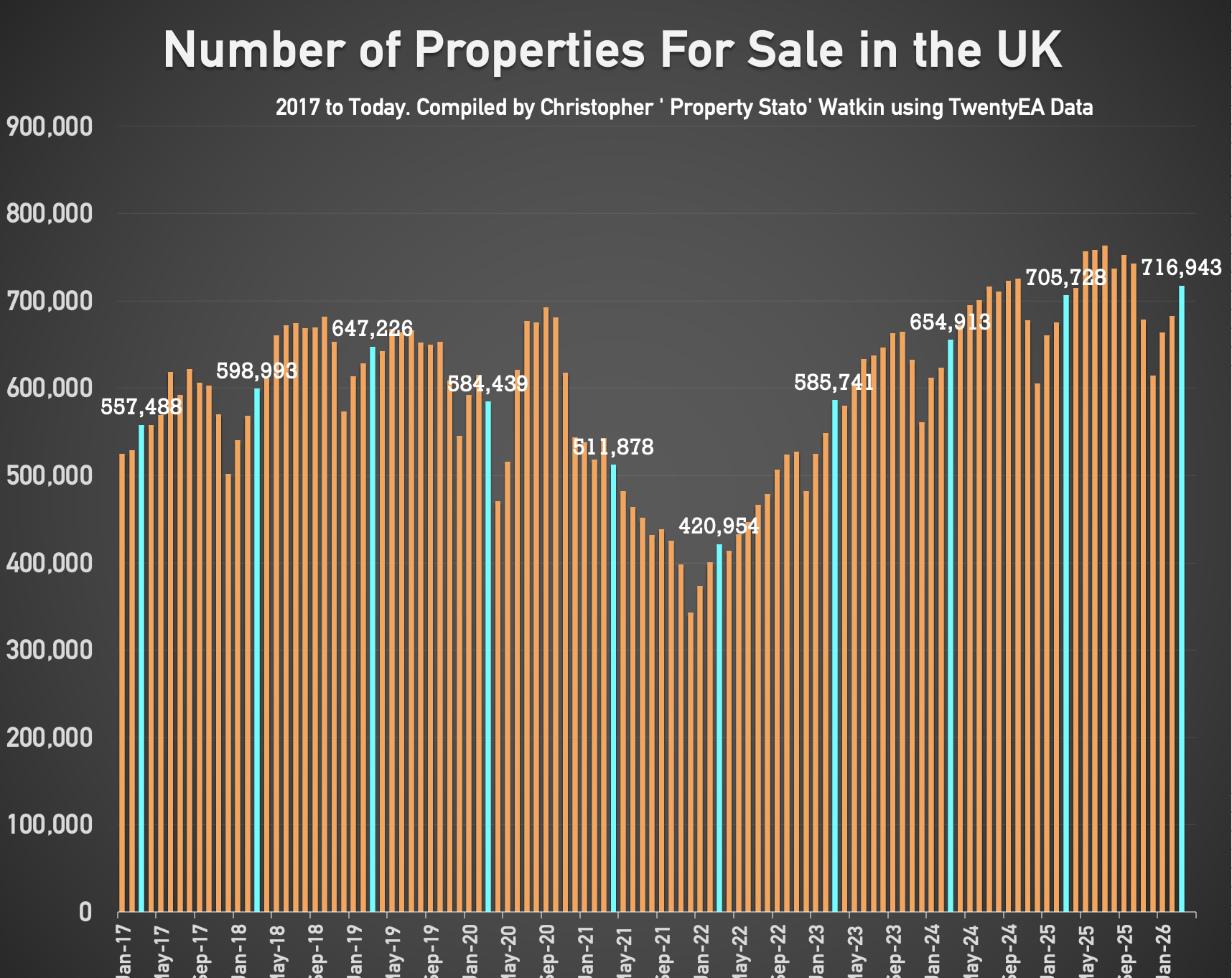

✅ stock levels

• 717k homes on the market as of April 1, 26. (706k – 1 Apr 25)

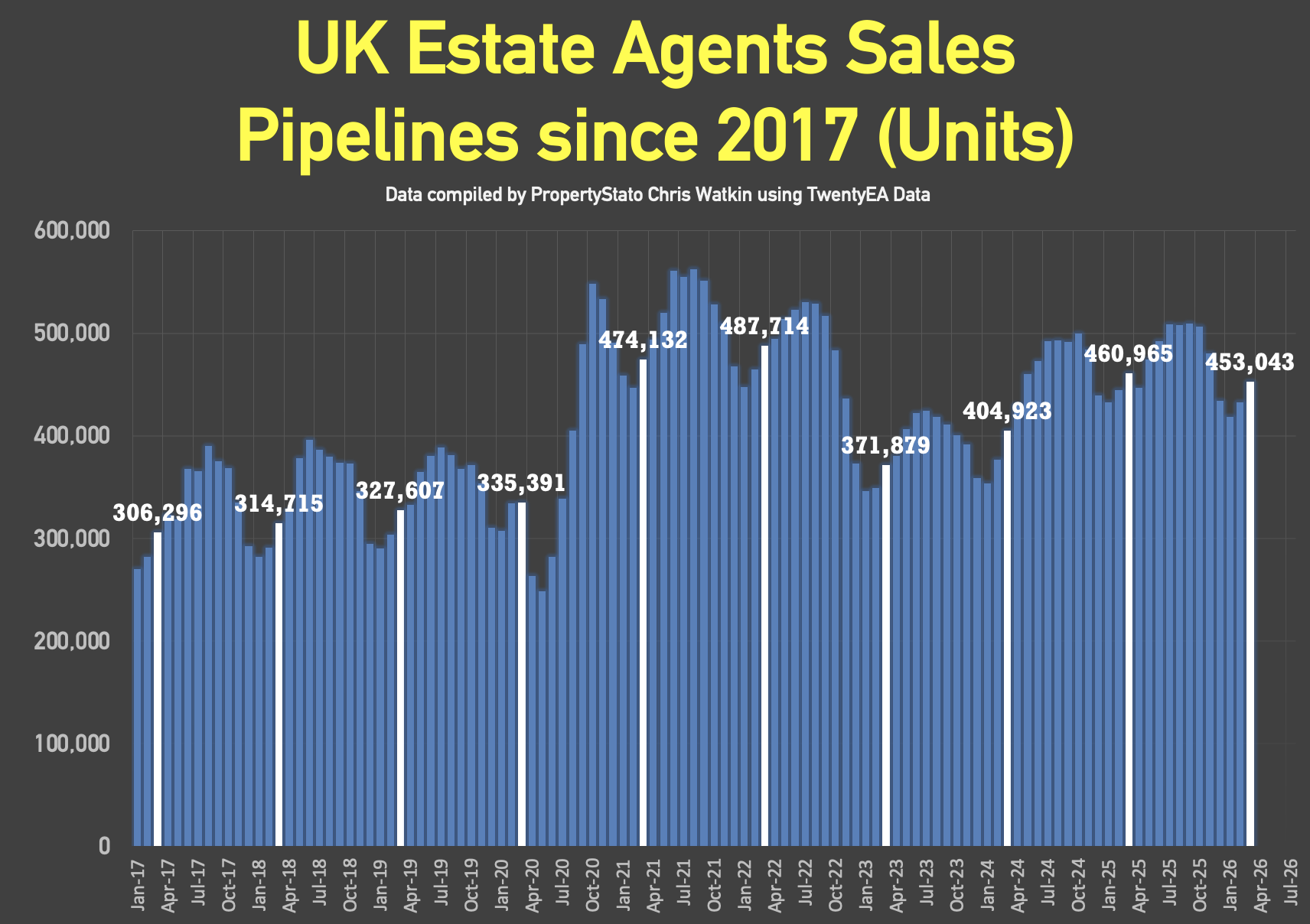

• 453k homes in the agent sales pipeline at 1 April 2026, slightly less than 12 months ago (461k) at 1 April 2025.

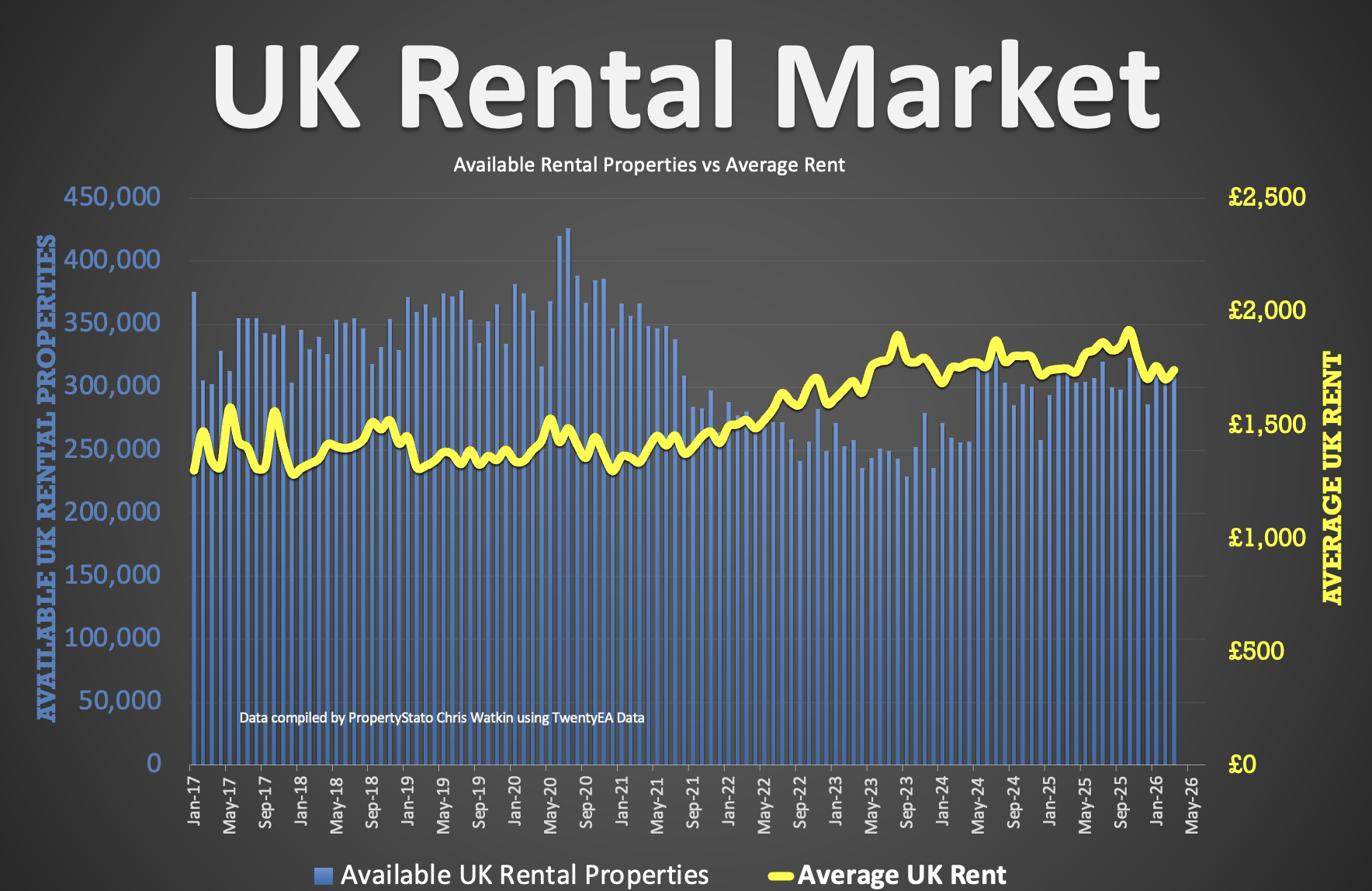

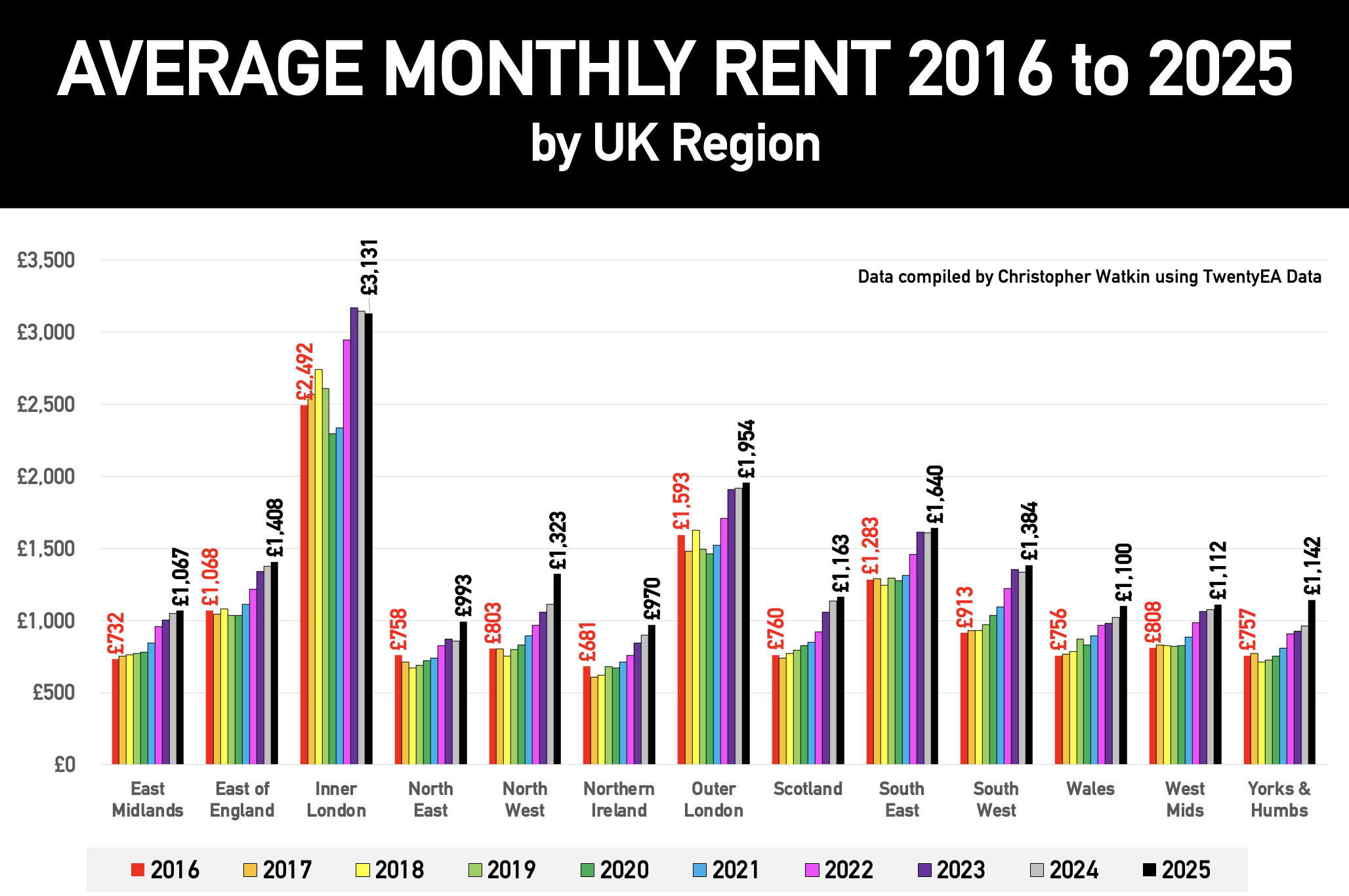

✅ UK rental data

• Average rent in March 2026 – £1,740 pcm (£1,747 in March 25)

• 312k of UK rental stock available to rent in March 26 (vs 313k in March 2025).

✅ local focus

pool